The Psychology of Risk and Decision-Making

Regret propels us forward and old habits drag us back, but companies still have to be profitable in the face of uncertainty and risk

By Adrienne Dawson

When thinking about risk, McCombs Assistant Dean and Distinguished Senior Lecturer Britt Freund likes to tell a story about an exchange he once overheard between executives from Exxon and Shell.

Exxon: “Why do you try to eat every cookie on the shelf?”

Shell: “Why do you pass by all of the cookies on the shelf?”

Every company, no matter the size or industry, has to contend with risk. The essential issue, say Freund and colleague Michelle Foss, the Chief Energy Economist with the Bureau of Economic Geology, is why people address risk so differently and what the implications are of that decision-making process.

“How could two large companies… look at the same data and come to drastically different conclusions about whether or not to engage in a risky decision?” asks Freund.

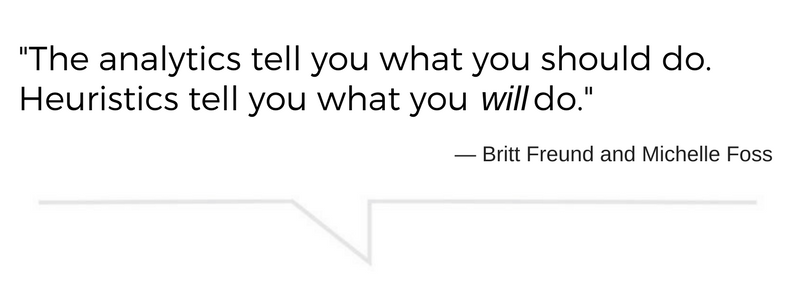

The reason, they say, is heuristics: The combination of past experience, corporate culture, and biases that allow people with similar information to make vastly different decisions. They can overwhelm projects when managers are pressured to make recommendations that fly in the face of their analyses. “The analytics will tell you what you should do,” says Freund. “Heuristics will tell you what you will do.”

Freund offers a real-world example:

It’s typical, he says, for managers to talk about a project’s budget as being +15/-10 of p-50. In other words, project costs can have an expected range of up to 15 percent more than the midpoint p-50 estimate (which becomes the project’s worst-case scenario, price-wise), or expenses can drop by as much as 10 percent below the midpoint (the best-case scenario).

Trouble is, recent studies examining the actual expenditure of major projects across various industrial companies found that the worst-case cost scenario isn’t a mere 15 percent higher than the midrange estimate, it’s actually three times the mid-range estimate. That means if the p-50 cost was estimated to be $4 billion, the project’s upper limit isn’t $4.6 billion — it’s actually closer to $12 billion.

But taking that figure to executives means project managers will “get laughed out of the room,” Freund says. They know the likelihood of certain risks and can calculate how expensive they’ll be if they materialize, but corporate culture — which drives the heuristics that human beings fall back on to make decisions — prevents managers from being honest about them if they want to see their projects come to fruition.

“We’re a mess,” Foss adds with a laugh. “Fortunately, we’ve learned how to conquer some of this.”

Addressing a project’s real risk up front requires an awareness of our own behaviors and biases, she says. A few key tips to keep in mind:

- Know the difference between technical and non-technical risk. Non-technical risk usually represents the variables that are harder to predict and control.

- Focus on risk mitigation. Foss offers, “For every risk you can’t control, there is still something that can be done to move it into your active-control column so that it’s no longer lurking around and haunting a project.”

- It’s ok to be risk-averse, but if you are, you’re going to leave a lot of cookies on the shelf. “That’s fine,” says Foss, “but then you better have something else that actually exceeds that cookie in potential value.”

- You cannot predict future events based on how often you’ve seen something happen in the past. “Nothing could be further from the truth,” she adds.

- Responses to risk create their own risks. Understand that a project’s environment is fluid, and it will change as new actions are taken.

- Aim for a robust decision, not an optimal one, Freund advises. “Physics is physics is physics, and you can model that… but the fuzzy human side gets so complicated and difficult to model that it overwhelms the idea of optimality.”

- Preserve your corporation’s memory. Foss cautions, “Too often, people move on, teams break apart, people retire, and you’re faced with making the same decision again.” And, likely, the same mistakes.

But the goal, they emphasize, is not to eliminate all risk. Says Freund, “If you find a way [to do that], you’ve probably eliminated a lot of the reward, too.”

Britt Freund and Michelle Foss spoke at The University of Texas at Austin as part of the Texas Enterprise Speaker Series on May 5, 2017. To hear more about recognizing and mitigating risk, watch the video below.

Originally published at www.texasenterprise.utexas.edu on May 31, 2017.

About this Post

Share: